Ramesh S Arunachalam

Rural Finance Practitioner

Dear Doug

Thanks for taking the time to clarify and really appreciate it! I attempt to provide my (final?) detailed response to your response. Again, much appreciate the work of CMF…and my raising issues does not take away the excellent work done by you all…I am such a regular reader of the research that you do…so please do take my comments for what they are worth and what they are not…

Your Stated Difficulty in Calculating Effective Interest Rates: Your point is well taken on the aspect of effective interest rates (EIR’s) – there are genuine difficulties in getting this information but I am sure that you will agree that any access to finance study will have limited utility, if it does not present information on effective interest rates.

Why is this so?

All of us have access to finance but at differential rates of interest and therefore, we need to understand the effective rates of interest (EIR’s) for the various sources. Only then, can we come to an informed judgment about the quality of access to finance and not mere access to finance. For example, for a medical emergency, even a very high cost informal loan may be classified as high quality access on the basis of the (very short) lead times to access the loan as it has the potential to perhaps save life. Likewise, a bullet 120 day period loan at a higher rate of interest may be preferable to a standardized 52 week MFI loan – as the potential of the former to satisfy working capital needs and suit the clients’ cash flows is perhaps better. Therefore, it becomes imperative, to understand all terms and conditions including effective interest rates when comparing alternative sources of finance…I am sure you will agree with this…

That said, forgive me, but I am unable to accept the argument that because it is difficult to calculate, we omit something that is as fundamental and as important as interest rates in an access to finance study…I would like to volunteer to help CMF in this if the raw data is available or can be compiled. I have a software tool (self created) by which we can compute the EIR’s fairly accurately in quick time. I have time in March and am happy to do it for you for the loans that you have data on…Do e mail or call me if you would like to take up my offer…

Additionally, people like Daniel Rozas, perhaps correctly feel, that the terms and conditions of friends/family who lend (for and without interest) are perhaps much more lenient (also long in tenor) in terms of several factors and therefore, should be analysed and presented separately in any access to finance study. It would be interesting to see what results the study throws up when friends/family as a category are selected out and presented separately – it would also be useful to understand the terms and conditions of friends as lenders of money…

In the same study, while admittedly difficult, we calculated the effective interest rates…rather laboriously…please see tables and figures below…

Inability to Pinpoint Sources of Cash for Loan Repayment: Likewise, it is important to understand the sources of cash for repayment as I have often come across clients borrowing from one source to repay another and also taking a 2nd/3rd loan to pay off the first and this does not take them anywhere…in the medium and long term…I just wanted to understand this aspect with regard to the study…I am sure you will agree that it would be important to know this…Much of the present crisis has been caused by huge levels of indebtedness with very little genuine repayment capacity… as Dr Y V Reddy, Mr Aditya Puri and others have regularly remarked…I felt your study could have provided valuable information to the world on this critical aspect…especially because it was conducted in AP

The Choice of Sampled Districts and The Exclusive Rural Focus: On the point of the districts, I am sorry but I missed figure 15 and my profuse and humble apologies - yes, the districts names can be got from there but I would have still preferred you coming out and saying that this study was conducted in “such and such districts”…for such and such reasons. I found it very difficult to read the fine print as well… I still feel that irrespective of the reason, the inability to survey and include highly saturated districts like Krishna[i], Guntur, East/West Godavari, Nellore, Kurnool, Khamman make the findings of the study less representative. I am sure that your study would have had very different results if some of these highly saturated districts, with lots of MFIs and multiple lending, had been included.

Please look at the following article (http://www.microfinancefocus.com/content/microfinance-crisis-case-hidden-city) which looks at urban/peri-urban clients and shows a significant difference in incidence of multiple borrowing and the like…

On the issue of the study being representative and also stating the exclusion of the urban areas, I still feel that it could have been presented in a straight forward manner…

I am not nitpicking but please note that depending on the depth to which a person gets into, the impressions about the study could be very different.

Therefore, I would have preferred the study to have been titled – “Access to Finance in Rural Andhra Pradesh”.

This title would also have explicitly told everyone that the study excludes urban areas…

Further, the point about NABARD not wanting to survey urban areas is perhaps understandable and also your point of therefore leaving out urban areas is well appreciated. However, the fact of the matter is that this survey does not cover urban areas where MFIs grew and proliferated at a frantic pace and where multiple, ghost and over lending was rampant. Therefore, the lack of urban respondents indeed severely limits any inference with regard to multiple lending and associated aspects in Andhra Pradesh and I am sure you would agree with this… Please look at the following article (http://www.microfinancefocus.com/content/microfinance-crisis-case-hidden-city) which looks at urban/peri-urban clients and shows a significant difference in incidence of multiple borrowing and the like…

Lack of Information About Sources of Funds for Friends: Again, knowledge about the sources of funds for the friends who lent for interest would have thrown light on whether - as Mr N Srinivasan has argued - clients were engaged in using (benami or other) loan money for money lending as an enterprise. Please see my post on agents (http://microfinance-in-india.blogspot.com/2011/01/broker-agent-in-indian-micro-finance.html) in Tamilnadu where MFIs themselves admit this…Hence I raised this issue…

The Positioning of The Study: And on the study being presented as a fresh study on AP, I am sorry but I beg to differ. Apart from the manner in which it was introduced in the CGAP blog and also the timing of its introduction, there are e mails from people close to CMF which have positioned the study rather incorrectly…I can share these with you…but the point is not to fault any one individual…so let us leave it at that…as I have made my position rather clear…

Thanks once again and I am grateful for the time taken by you and the CMF team to do the study and also respond to me...

Thanks

Warm Regards

Ramesh

Originals Post:

CMF Study on Access to Finance in Andhra Pradesh: Some Observations for The RBI and Other Stakeholders…

http://microfinance-in-india.blogspot.com/2011/01/cmf-study-on-access-to-finance-in.html

CMF Response:

Response to Criticism of "Access to Finance in Andhra Pradesh"

http://www.indiadevelopmentblog.com/2011/01/response-to-criticism-of-access-to.html

Rural Finance Practitioner

Dear Doug

Thanks for taking the time to clarify and really appreciate it! I attempt to provide my (final?) detailed response to your response. Again, much appreciate the work of CMF…and my raising issues does not take away the excellent work done by you all…I am such a regular reader of the research that you do…so please do take my comments for what they are worth and what they are not…

Your Stated Difficulty in Calculating Effective Interest Rates: Your point is well taken on the aspect of effective interest rates (EIR’s) – there are genuine difficulties in getting this information but I am sure that you will agree that any access to finance study will have limited utility, if it does not present information on effective interest rates.

That said, many other studies that have looked at access to finance (Odisha Study by Access Development Services, APMAS Studies and even an UNTRS/FAO studies on fisheries that I was involved with), despite the real time difficulties, did try and calculate the effective interest rates and in many cases, at least provided a range of the effective interest rates for the various sources of finance. Please see example tables, below, reproduced from A Study of SHGs and their Federations in Odisha, For TRIPTI, Access Development Services, New Delhi

All of us have access to finance but at differential rates of interest and therefore, we need to understand the effective rates of interest (EIR’s) for the various sources. Only then, can we come to an informed judgment about the quality of access to finance and not mere access to finance. For example, for a medical emergency, even a very high cost informal loan may be classified as high quality access on the basis of the (very short) lead times to access the loan as it has the potential to perhaps save life. Likewise, a bullet 120 day period loan at a higher rate of interest may be preferable to a standardized 52 week MFI loan – as the potential of the former to satisfy working capital needs and suit the clients’ cash flows is perhaps better. Therefore, it becomes imperative, to understand all terms and conditions including effective interest rates when comparing alternative sources of finance…I am sure you will agree with this…

That said, forgive me, but I am unable to accept the argument that because it is difficult to calculate, we omit something that is as fundamental and as important as interest rates in an access to finance study…I would like to volunteer to help CMF in this if the raw data is available or can be compiled. I have a software tool (self created) by which we can compute the EIR’s fairly accurately in quick time. I have time in March and am happy to do it for you for the loans that you have data on…Do e mail or call me if you would like to take up my offer…

Additionally, people like Daniel Rozas, perhaps correctly feel, that the terms and conditions of friends/family who lend (for and without interest) are perhaps much more lenient (also long in tenor) in terms of several factors and therefore, should be analysed and presented separately in any access to finance study. It would be interesting to see what results the study throws up when friends/family as a category are selected out and presented separately – it would also be useful to understand the terms and conditions of friends as lenders of money…

In the fisheries sector, in Enhancing Financial Services Flow to Small Scale Marine Fisheries Sector a study done for UNTRS/FAO (2007) in Southern India as part of the UNTRS project, we found that fishermen saved by giving their excess money (sometimes, they have this huge liquidity when they may have caught a special variety of fish – hammer head shark for instance) as medium/long term loans to their peers. In fact, many of the women said that they preferred this kind of loaning to avoid the money from being wastefully spent away by their husbands…such were loans were also made for safety purposes…

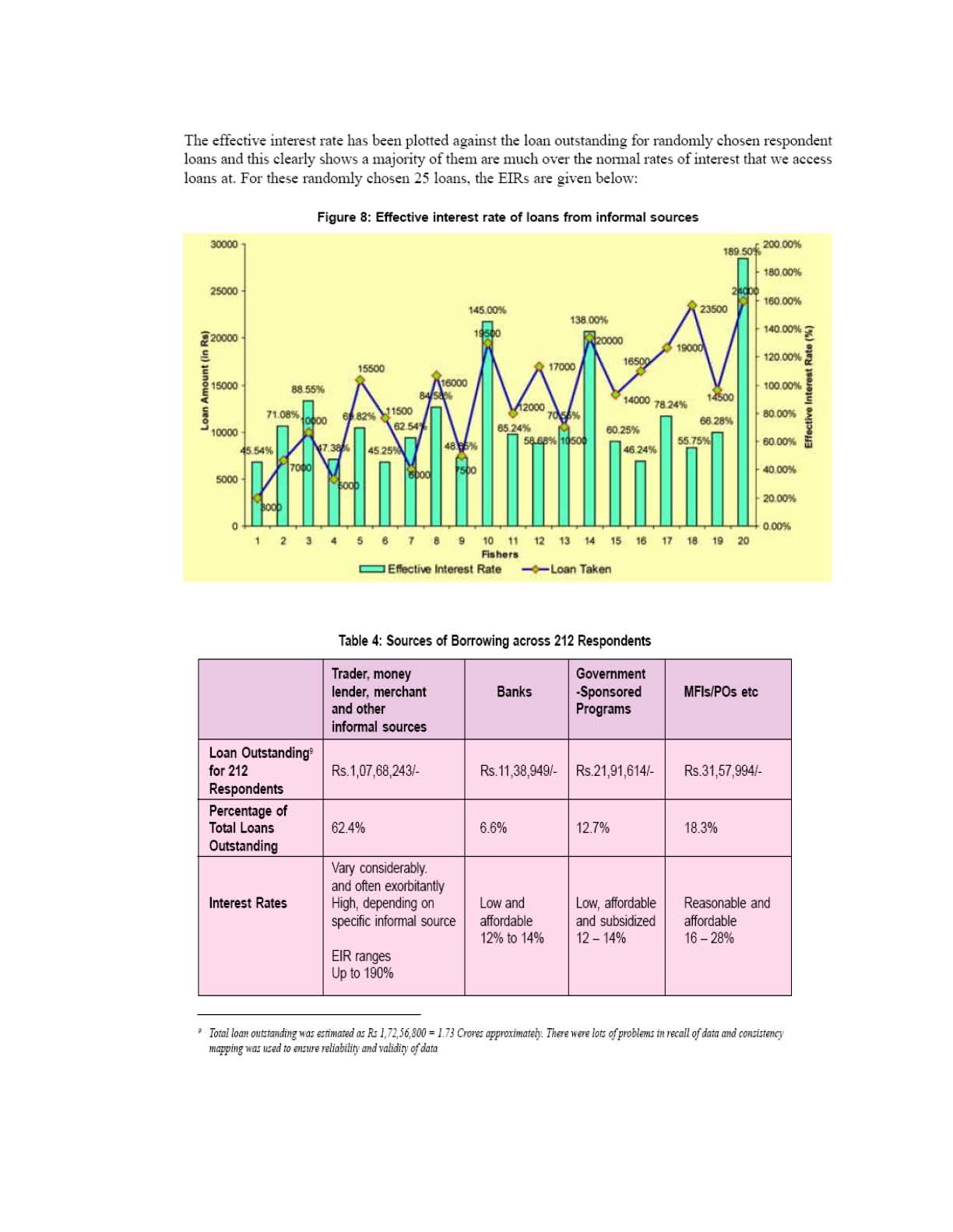

In the same study, while admittedly difficult, we calculated the effective interest rates…rather laboriously…please see tables and figures below…

We had even tried to do an attribute ranking among the respondents with great difficulty – see relevant table below…I do however agree that the above study was much smaller in terms of sample size…

Therefore, come what may, it is imperative that any access to finance study provide at least some information on the effective interest rates…I am sure that you will recognize this crucial aspect…That was the larger point I am making…

Inability to Pinpoint Sources of Cash for Loan Repayment: Likewise, it is important to understand the sources of cash for repayment as I have often come across clients borrowing from one source to repay another and also taking a 2nd/3rd loan to pay off the first and this does not take them anywhere…in the medium and long term…I just wanted to understand this aspect with regard to the study…I am sure you will agree that it would be important to know this…Much of the present crisis has been caused by huge levels of indebtedness with very little genuine repayment capacity… as Dr Y V Reddy, Mr Aditya Puri and others have regularly remarked…I felt your study could have provided valuable information to the world on this critical aspect…especially because it was conducted in AP

The Choice of Sampled Districts and The Exclusive Rural Focus: On the point of the districts, I am sorry but I missed figure 15 and my profuse and humble apologies - yes, the districts names can be got from there but I would have still preferred you coming out and saying that this study was conducted in “such and such districts”…for such and such reasons. I found it very difficult to read the fine print as well… I still feel that irrespective of the reason, the inability to survey and include highly saturated districts like Krishna[i], Guntur, East/West Godavari, Nellore, Kurnool, Khamman make the findings of the study less representative. I am sure that your study would have had very different results if some of these highly saturated districts, with lots of MFIs and multiple lending, had been included.

Please look at the following article (http://www.microfinancefocus.com/content/microfinance-crisis-case-hidden-city) which looks at urban/peri-urban clients and shows a significant difference in incidence of multiple borrowing and the like…

On the issue of the study being representative and also stating the exclusion of the urban areas, I still feel that it could have been presented in a straight forward manner…

· If one were to look at the title of the paper, one comes to the conclusion that this is a study on access to finance in Andhra Pradesh.

· If one were to look at the executive summary, the impression changes to the study being an access to finance study in rural Andhra pradesh.

· Now, when one gets to the fine print…(and not everyone may read the real fine print) - one would see your comments on it being representative of rural AP minus Krishna.

I am not nitpicking but please note that depending on the depth to which a person gets into, the impressions about the study could be very different.

Therefore, I would have preferred the study to have been titled – “Access to Finance in Rural Andhra Pradesh”.

This title would also have explicitly told everyone that the study excludes urban areas…

Further, the point about NABARD not wanting to survey urban areas is perhaps understandable and also your point of therefore leaving out urban areas is well appreciated. However, the fact of the matter is that this survey does not cover urban areas where MFIs grew and proliferated at a frantic pace and where multiple, ghost and over lending was rampant. Therefore, the lack of urban respondents indeed severely limits any inference with regard to multiple lending and associated aspects in Andhra Pradesh and I am sure you would agree with this… Please look at the following article (http://www.microfinancefocus.com/content/microfinance-crisis-case-hidden-city) which looks at urban/peri-urban clients and shows a significant difference in incidence of multiple borrowing and the like…

Lack of Information About Sources of Funds for Friends: Again, knowledge about the sources of funds for the friends who lent for interest would have thrown light on whether - as Mr N Srinivasan has argued - clients were engaged in using (benami or other) loan money for money lending as an enterprise. Please see my post on agents (http://microfinance-in-india.blogspot.com/2011/01/broker-agent-in-indian-micro-finance.html) in Tamilnadu where MFIs themselves admit this…Hence I raised this issue…

The Positioning of The Study: And on the study being presented as a fresh study on AP, I am sorry but I beg to differ. Apart from the manner in which it was introduced in the CGAP blog and also the timing of its introduction, there are e mails from people close to CMF which have positioned the study rather incorrectly…I can share these with you…but the point is not to fault any one individual…so let us leave it at that…as I have made my position rather clear…

Thanks once again and I am grateful for the time taken by you and the CMF team to do the study and also respond to me...

Thanks

Warm Regards

Ramesh

Originals Post:

CMF Study on Access to Finance in Andhra Pradesh: Some Observations for The RBI and Other Stakeholders…

http://microfinance-in-india.blogspot.com/2011/01/cmf-study-on-access-to-finance-in.html

CMF Response:

Response to Criticism of "Access to Finance in Andhra Pradesh"

http://www.indiadevelopmentblog.com/2011/01/response-to-criticism-of-access-to.html

[i] I also think that much of the randomness was lost when Krishna district was omitted, whatever be the reason…

Hi Ramesh!

ReplyDeleteI did comment on the CMR study on the India Development Blog, but for reasons known to them, it was not published. Here's the comment:

Some reactions:

1. "We included urban areas in our initial proposal to NABARD, but, understandably, given NABARD's mandate, they requested us to focus on rural areas only."

Since we all know that MFIs operationally are essentially an urban phenomenon, what this admission tantamount to is conceding that it is not reflective of the MF sector. If such a study was used for your in-house purposes, I sure you would have avoided the attention you are now getting. But it was not. Once published and other researches, blogs and articles start quoting the contents as a reflecting the MF industry, it not only immediately warrants attention but also a rejoinder as did the Ramesh Arunanchalam blog.

2. "Actually, it is -- with the caveat mentioned in the document (and in the posting), that it should be considered representative of rural Andhra Pradesh with the exception of Krishna district."

Is or isn't Krishna a part of AP? Since it is, what exactly is the rationale for excluding Krishna? Is it because if included the findings will embarrass the sector as the district was the centre of a backlash against the MF industry some years ago. Methodologically, the exclusion of Krishna suggests to me it no longer remains random as you claim!

3. "The study does not include information on interest rates."

Tell me something. Can you do a study on omelets by excluding egg as an ingredient? That's exactly what your admission apparently does. CMF must be considering readers as imbecile idiots if they were to accept your arguments that differences like lump-sum and installment payment provided obstacles to ascertaining effective interests. Any researcher's curiosity would be arouse to have an insight what's the difference in terms of effective interest rates paid by the borrower repaying the entire principal as a lump sum at the end of the loan and those paying by installments. It is amazing that it did not to CMF who instead considered them an obstacle to ascertaining effective interest rates. It looks to me additionally that the provision of information on MFI interest rates would be equally embarrassing to the MF industry just as Krishna was to the sample. Both are glaring omissions that raise questions on the robustness of the methodology pursued.

4. "The study does not mention how people got the money to repay their loans." I remain speechless for the same reason mentioned under item 3 of my reactions. Most probably, if CMF did, it would have exposed how MFIs manage their 99% repayment rates like people selling their productive assets like goats, house utensil, mangalsutra etc. Money is indeed fungible. But within the context of coercive recovery practices of MFIs, the it ceases to be fungible any more.

I am sorry to say that if consultants and researchers had played their role they are expected to perform, perhaps the MF industry would not find itself in such a crisis that it confronts today. The least we expect from CMF is to admit that there were certain methodological shortfalls. But this rejoinder came as a disappointment.

MFI Watch

http://devconsultgroup.blogspot.com/

Dear Ramesh,

ReplyDeleteThanks for the additional comments. With regard to the calculation of interest rates, please do feel free to download the data and take a shot at it. As mentioned in the report itself, all of the data along with an English version of the questionnaire and detailed instructions on how to get started in analyzing the data in R and Stata are available on the CMF website at http://www.ifmr.ac.in/cmf/resources.html.

As I wrote in the blog though, I don't think this exercise would be very fruitful. For those loans from informal sources in which the principal was paid back at the end of the loan, calculation of interest rates is a straightforward task. For loans in which this is not the case, it simply isn't possible to calculate the effective interest rate unless there is something I am missing here. I would be curious to see how this was done for the other surveys. I attempted to find the questionnaires and data online but was unable to.

As an interesting aside, I many people have misinterpreted our results as implying that the "big bad moneylender" is still preying on the rural poor in Andhra Pradesh. (A view we did nothing to encourage in the report.) For those loans from informal sources for which we were able to calculate the effective interest rate (even those from sources described as moneylenders) the effective interest rates tended to be much lower than what most people think they are.

Dear Rajan,

Your comment is there on the India Development Blog under the post "Malegam Committee Releases Recommendations". Not sure why it's under that post rather than the post with the response to Ramesh but it certainly wasn't because we moved it. We don't moderate comments on the blog except to remove things like spam.

Dear Doug

ReplyDeleteThanks and yes, I will try and let you when I have been able to look at it. Thanks. For the study I was involved the questionnaires and data are not public...there is a confidentiality clause but I have methodology note that gave rules of thumb for calcultaing eirs with examples for informal loans and I will take permission and try and send that to you. I need to check on the Odisha study with people who did the study and I will do so and get back

The point about big bad money lender was made by Ajay and I will let him answer that...

Thanks again Doug. Time to move on from this study...

Warm Regards

Ramesh